Insurance Claim Rules for Rideshare Periods

According to 2019 data collected by the Insurance Information Institute (III), California is ranked 10 out of all states with the highest number of uninsured motorists. The most common factor that has contributed to this problem is the cost of paying for personal auto insurance. Many people are unable to afford having to pay for expensive auto insurance since they have other monthly expenses to pay off.

Luckily, California has an automobile liability insurance program available to assist those with specific levels of income. The state hopes to achieve the objective of having drivers covered by offering affordable insurance options.

With that being said, it is important for all drivers, especially rideshare drivers, to acquire personal auto insurance. Rideshare drivers are on the road far more often than regular drivers, thus increasing the likelihood of getting into a motor vehicle accident. With personal auto insurance, a rideshare driver could acquire financial assistance in case they are at-fault for an accident and are required to provide compensation to the other party for damages.

In addition to personal insurance, it is a good idea to invest in rideshare insurance. Rideshare insurance is a unique form of insurance. It combines job security, as well as personal coverage. While Uber and Lyft have their own insurance policies, it is best to be fully covered from all angles.

If you’ve suffered a personal injury or had any damage done to your vehicle as a result of an Uber or Lyft accident, you may need help recovering compensation for your losses. At West Coast Trial Lawyers, our qualified Uber and Lyft accident lawyers have over 60 years of collective legal experience in handling personal injury cases. With our track record of recovering more than $1 billion in settlements for our clients, we are confident that we will deliver a good outcome to your case.

To schedule a free consultation, we welcome you to contact our 24/7 legal team by calling 213-927-3700 or filling out our quick contact form.

Do You Need Rideshare Insurance?

You may not think you need rideshare insurance until it is too late. Many do not know this, but your personal car insurance may not cover an accident that happened while you’re on the clock. In fact, your auto insurer may cancel your policy if they discover that you are using your car for work and haven’t disclosed that information to them. If you do have Uber or Lyft insurance, you may be unaware that there is a vital period where you may not be covered.

The coverage of your Uber or Lyft insurance is dependent on the time of the accident. In most cases, while waiting for a rider’s request, your coverage can include basic liability coverage. Basic liability insurance covers:

- $50,000 for bodily injury per person

- $100,000 for bodily injury per accident

- $25,000 for in property damage per accident

Most insurers provide rideshare insurance options. Generally, these options boost your personal policy and cover ridesharing issues. They’re included in your new policy as an “add-on” and there is no need for an entirely new separate policy. Understanding the process of disputing an Uber or Lyft damage is an important aspect of the claim.

Rideshare Periods

Uber and Lyft offer auto insurance to their rideshare drivers to protect them from a covered accident. However, each policy will be activated depending on what the rideshare driver was doing during the time of the accident. Both rideshare companies have provided a breakdown of what the rideshare driver is expected to receive based on the type of situation they are in. This includes the following:

- The rideshare driver is offline. If a rideshare driver was involved in a motor vehicle accident while they were not logged into their Uber or Lyft app, then they will not be granted coverage. They will have to rely on their own personal auto insurance for financial assistance.

- The rideshare driver is online and awaiting a ride request. If the rideshare driver was logged into an Uber or Lyft app and was waiting to receive a ride request during the time of the accident, then Uber or Lyft will provide third-party liability only if the rideshare driver’s personal auto insurance does not apply. This includes $50,000 per bodily injury, $100,000 per accident, and $25,000 in property damage per accident.

- The rideshare driver is online and has accepted a request or is on the way to pick up or drop off a rider. If the rideshare driver got into an accident while they were picking up or dropping off a rider, Uber and Lyft will provide a $1 million third-party, uninsured/underinsured motorist (UM/UIM) coverage, and contingent comprehensive and collision coverage.

Uber also offers Injury Protection, which is paid for by them, as well. Since the passage of Prop 22, rideshare (and delivery) drivers are now able to obtain Injury Protection insurance. This insurance will help cover Uber rideshare (or delivery) drivers who have sustained injuries in an accident while fulfilling rideshare-related tasks (or delivering orders). Benefits may include disability payments, medical bills, and survivor benefits.

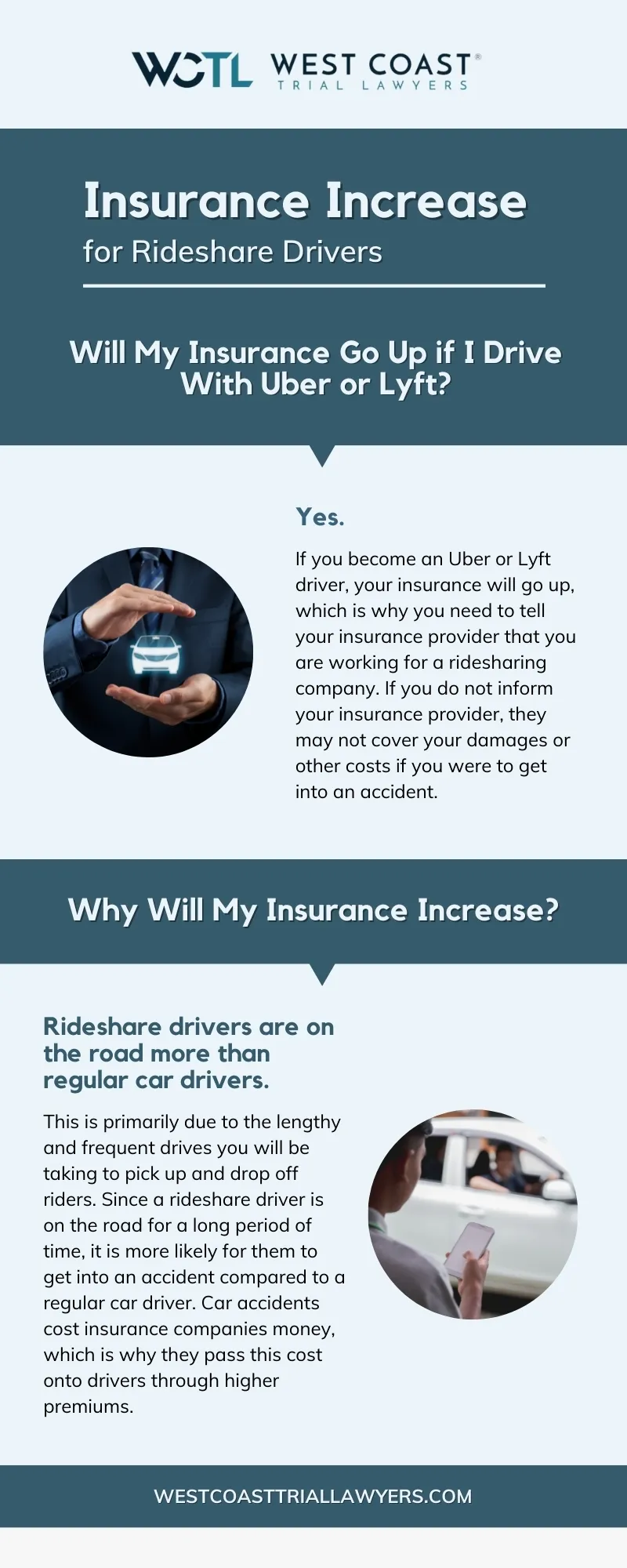

Will My Insurance Go Up if I Drive With Uber or Lyft?

If you become an Uber or Lyft driver, your insurance will go up, which is why you need to tell your insurance provider that you are working for a rideshare company. If you do not inform your insurance provider, they may not cover your damages or other costs if you were to get into an accident.

If you become an Uber or Lyft driver, your insurance will go up, which is why you need to tell your insurance provider that you are working for a rideshare company. If you do not inform your insurance provider, they may not cover your damages or other costs if you were to get into an accident.

Once you tell your insurance provider that you are working for a rideshare company, they will likely increase your premium. This is primarily due to the lengthy and frequent drives you will be taking to pick up and drop off riders. Since a rideshare driver is on the road for a long period of time, it is more likely for them to get into an accident compared to an average driver. Car accidents cost insurance companies money, which is why they pass this cost onto drivers through higher premiums.

Other than your insurance costs going up, driving for a rideshare company will have you switch insurance providers completely. The insurance industry has been fairly slow about adjusting to a rideshare driver’s needs. Instead of creating options for Uber and Lyft drivers, some insurance companies refuse to offer them coverage. A number of insurance carriers will not let you be insured with them if you are using your car for rideshare purposes. Even though your insurance carrier may not actually allow rideshare coverage, you need to inform them about your job anyway.

When you update your insurance plan, you should carefully read through the policy. There may be a gap in coverage when it comes to your car’s physical damage in an accident. Any coverage gaps could leave you paying for a bunch of out-of-pocket expenses if an accident occurs. While a coverage gap may be acceptable to you, you need to know whether it exists or not so that you can make an informed decision.

Available Damages After an Uber or Lyft Accident

If you are a victim of an Uber or Lyft accident, you will be eligible to file a personal injury claim against the party at-fault for your losses. This will help prevent you from falling into a financial burden. To make sure all of your losses have been acknowledged, our Uber and Lyft accident lawyers will assess your case to categorize your damages into economic damages and non-economic damages.

Economic damages are referred to as out-of-pocket expenses that have monetary value. This includes medical bills, lost wages, loss of past and future earnings, costs of increased insurance premiums, loss of household services, costs of repairing or replacing your vehicle, loss of employment opportunities, and more.

Non-economic damages are identified as non-monetary losses. This includes loss of companionship and love, diminished earning capacity, loss of support, emotional distress, skin scarring, pain and suffering, and so on.

A victim who has suffered an injury due to an Uber or Lyft accident may question whether they may be eligible to receive punitive damages. According to California Civil Code 3294, punitive damages may only be granted if the defendant’s actions were intentional or malicious. If the victim is able to provide proof of the defendant’s willful misconduct, then they will be granted punitive damages as part of their settlement offer.

West Coast Trial Lawyers Is Here to Help

Victims of an Uber or Lyft accident are welcomed to contact our 24/7 legal team at West Coast Trial Lawyers. Our experienced Uber and Lyft accident lawyers are determined to get you a fair settlement offer that will help cover your losses.

Our personal injury law firm provides no-cost, risk-free consultations. Contact us today by calling 213-927-3700 or filling out our contact form to start on your claim.